forbidden words: discussion of federal policies — Economic Prosperity and Trade Policy

discussion of federal policies: Economic Prosperity and Trade Policy

from U.S. Department of State Policy Issues: Economic Prosperity and Trade Policy

2021-2025 ARCHIVED CONTENT

You are viewing ARCHIVED CONTENT released online from January 20, 2021 to January 20, 2025.

Content in this archive site is NOT UPDATED, and links may not function.

For current information, go to www.state.gov.

Policy Issues – Economic Prosperity and Trade Policy

The Economic Bureau (EB) comprises an extensive group of officers focused on building a strong U.S. economy that creates jobs and underpins national security. A central element of that vision is the pursuit of free, fair, and reciprocal trade.

Our officers highlight economic considerations in policy formulation. They build the relationships needed to expand commercial ties that drive American prosperity. Our role in policy also extends to implementing sanctions against terrorists, human rights abusers, and corrupt officials. The Department of State additionally works to strengthen property rights and contract enforcement, competition policies, sound commercial law, and the protection and enforcement of intellectual property rights around the world. The Department’s efforts aim to ensure that the United States remains the world’s strongest and most dynamic economy.

Read more about what specific bureaus and offices are doing to support this policy issue:

Bureau of Economic and Business Affairs (EB): EB works to create jobs at home, boost economic opportunities overseas, and make America more secure. It promotes a strong American economy by ensuring a level-playing field for American companies doing business around the world and attracting foreign investors to create jobs in America. Read more about EB

Trade Policy and Negotiations (EB/TPN): The TPN staff — in the Bilateral Trade Affairs, Multilateral Trade Affairs, Agricultural Policy, and Intellectual Property Enforcement offices — works to open markets for U.S. products and services overseas and strengthen U.S. trade relationships around the world.

from — Economic Prosperity and Trade Policy – United States Department of State. (2024, July 17). United States Department of State.

~ ~ ~

One Tariff, Many Questions: Trade Policy Uncertainty Under Trump

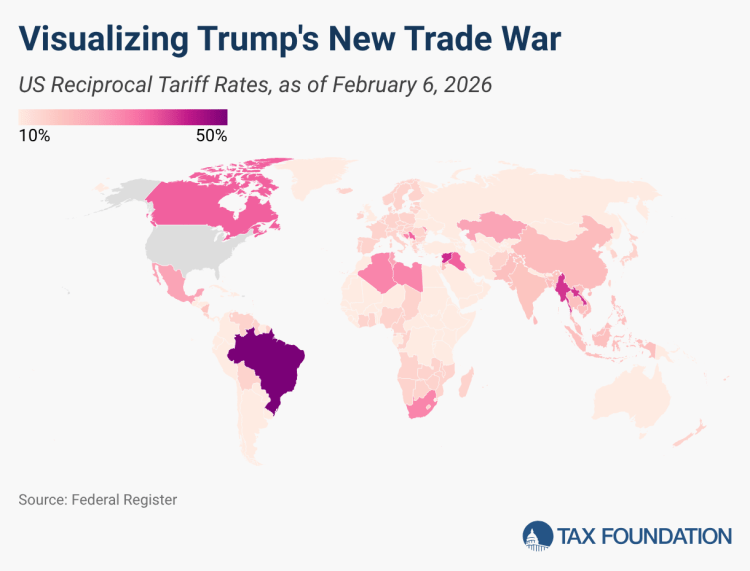

Ten percent reciprocal tariffs worldwide. That was President Trump’s response on February 20 to a US Supreme Court decision declaring the tariffs he imposed under the International Emergency Economic Powers Act (IEEPA) illegal.

At first glance, the announcement appears to simplify an increasingly complex tariff regime. But in reality, it introduces yet another layer of uncertainty.

The facts

On February 20, President Trump issued an executive order declaring that all executive orders relying on IEEPA would no longer be in effect. This decision rescinded all reciprocal tariffs imposed on countries around the world through executive orders and their amendments; the additional reciprocal tariffs imposed on Brazil; additional tariffs on India related to oil imports from Russia; tariffs on countries importing oil from Venezuela or Iran and on countries exporting oil to Cuba; and the so-called fentanyl tariffs imposed on China, Mexico, and Canada. At the same time, the exclusion of de minimis imports from the list of tariff-exempt products was reaffirmed.

Through a White House fact sheet released that day, the administration replaced reciprocal tariffs with a uniform 10 percent tariff applied to all countries, invoking Section 122 of the 1974 Trade Act. This measure is explicitly temporary, limited to 150 days. A revised list of exempted products was also published.

Importantly, sector-specific tariffs—including those on copper, steel, aluminum, automobiles, and lumber—remain in place.

On February 21, President Trump announced via social media a possible increase in the uniform tariff to 15 percent. At the time of this writing, however, that increase has not taken effect.

How were countries affected?

To assess the impact of these changes, we updated the CGD Tariff Tracker to calculate changes in effective tariff rates (ETRs)—the weighted average tariff actually applied to a country’s exports, taking into account product-level exemptions and sector-specific levies. Figure 1 compares the ETRs before and after the most recent policy shifts.

Figure 1. Effective tariff rates before and after recent US policy announcements

As shown by countries’ positions relative to the 45-degree line, no country faces higher ETRs under the new regime; most are either unaffected or face a lower ETR. Three factors explain this result:

- Before February 20, the baseline reciprocal tariff for many countries was already 10 percent; no country faced a lower reciprocal tariff.

- The new list of exempted products differs only marginally from the previous one.

- We assume that countries with existing and pending trade agreements will also face a 10 percent reciprocal tariff until either a new policy is announced or the temporary authority expires in July, whichever comes first. In other words, even if a country has agreed to a reciprocal tariff above 10 percent in a trade deal, we assume the agreed tariff is not applied while the temporary regime remains in place.

Who benefits most?

Which countries see the largest decline in effective tariffs—that is, which lie farthest above the 45-degree line? Two groups stand out: the BRIC countries excluding Russia, and countries that previously faced very high tariffs after failing to secure trade deals with the US.

Among the BRIC countries:

- Brazil faced a 50 percent reciprocal tariff, which, after exceptions, translated into an ETR of 26.3 percent.

- China was subject to additional Trump-era tariffs totaling about 20 percent, partly driven by fentanyl-related tariffs.

- India announced a trade deal in early February that would have reduced its reciprocal tariff from 50 to 18 percent. However, negotiations were paused on February 23 in light of recent developments.

Among countries without trade deals, Laos and Myanmar stand out. Both faced ETRs close to 40 percent, reflecting stalled negotiations and limited alignment with US trade and security priorities.

What about countries that had negotiated deals?

The table below summarizes the status of recent trade agreements and their agreed reciprocal tariffs. Most involved tariff rates well above 10 percent.

If the new tariff regime stays in place, many of these agreements will effectively need to be reopened. Indeed, India has paused trade talks, and the European Union has signaled a freeze on ratification of the recently concluded agreements.

The threat of heightened uncertainties

Do stable or declining ETRs mean that countries—and the global economy—are better off? The answer is a resounding NO.

Enormous uncertainty defines the current trade regime, weighing heavily on governments’ and firms’ ability to make investment and production decisions. Consider just a few open questions:

- How will US importers respond? In 2025, expectations of tariff increases led firms to frontload imports in the first half of the year, followed by a sharp decline once tariffs took effect in August. Will firms rush to frontload imports again, while the current regime lasts? Or will the costs imposed by pervasive uncertainty significantly discourage trade, dragging down both US growth and global demand?

- What happens to previously negotiated trade deals? Even if reciprocal tariffs settle at 10 percent, what becomes of the non-tariff concessions—most notably large investment commitments into the US—that partner countries agreed to? Recent developments strongly incentivize a wait-and-see approach over renewed negotiations.

- What about sub-Saharan Africa? Many African countries benefit from the African Growth and Opportunity Act (AGOA), which exempts numerous exports from US tariffs. But AGOA is set to expire at the end of this year. What tariffs will replace AGOA? How can investors (in both the US and African countries) make credible trade and investment plans when the post-AGOA regime remains entirely unclear? These uncertainties don’t bode well for Africa’s economic prospects.

- Will uncertainty accelerate trade fragmentation? Heightened US-driven uncertainty may inject new momentum into alternative trade blocs and deepen shifts away from the US as both a trade and a financial partner. It is difficult to see how the US ultimately benefits from such dynamics

A final word

Uncertainty is the enemy of trade and investment. Firms cannot commit capital when the rules of the game change every few weeks. A final figure underscores the point: US trade policy uncertainty has returned to levels last seen in April 2025, when the US administration launched a rapid and destabilizing sequence of tariff changes that continue to disrupt the global economy.

from — Rojas-Suarez, L., & Albe, I. (2026, February 25). One Tariff, Many Questions: Trade Policy Uncertainty Under Trump. Center for Global Development. Retrieved February 25, 2026

~ ~ ~

From TaxFoundation.org

Tariff Tracker: Impact of Trump Tariffs & Trade War by the Numbers

Impact of Trump Tariffs by the Numbers

President Trump’s Imposed and Threatened Tariffs, Topline Preliminary Estimates

| $700 | $668.1 | −0.2% | 0.1% | -154,000 |

|---|

Key Findings

- President Trump imposed IEEPA tariffs on US trading partners in 2025, including China, Canada, Mexico, and the EU. In addition, he has threatened and imposed Section 232 tariffs on autos, heavy trucks, steel, aluminum, lumber, furniture, semiconductors, pharmaceuticals, and copper, among others.

- The Supreme Court recently ruled in a 6-3 decision in Learning Resources Inc. v. Trump and V.O.S. Selections v. United States that “IEEPA does not authorize the President to impose tariffs.”

- President Trump responded by signing an executive order that would impose a 10 percent tariff on all countries under Section 122 with exemptions, effective February 24, 2026. On February 21, 2026, he threatened to increase the Section 122 rate to 15 percent, but it took effect at the announced 10 percent rate. We estimate this new tariff would apply to $1.2 trillion worth (34 percent) of annual imports. The tariff is scheduled to expire after 150 days.

- In 2025, the Trump tariffs amounted to an average tax increase per US household of $1,000. After the IEEPA tariffs were struck down, we estimate the President’s remaining new tariffs under Section 232 will increase taxes per US household by $400 in 2026. The Section 122 tariffs will increase this household burden by about $200 to $600 in 2026.

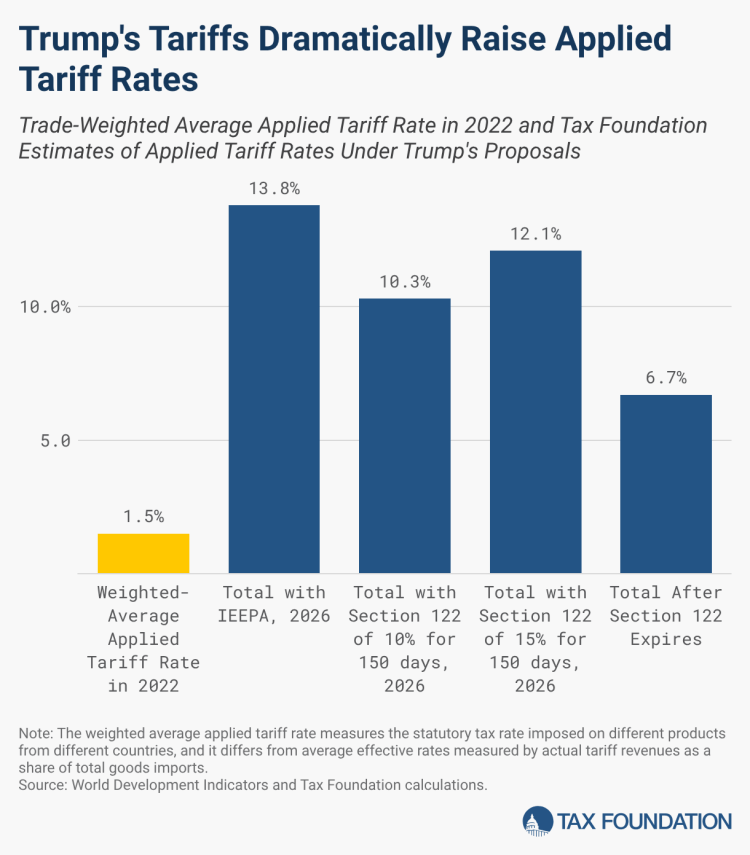

- We estimate with the IEEPA tariffs being ruled illegal, the remaining Section 232 tariffs imposed in 2025 increase the weighted average applied tariff rate on all imports to 6.7 percent in 2026, down from 13.8 percent under the IEEPA tariffs. While the 10 percent Section 122 tariffs are in effect, we estimate this rises to 10.3 percent, and then falls to 6.7 percent after the Section 122 tariffs end.

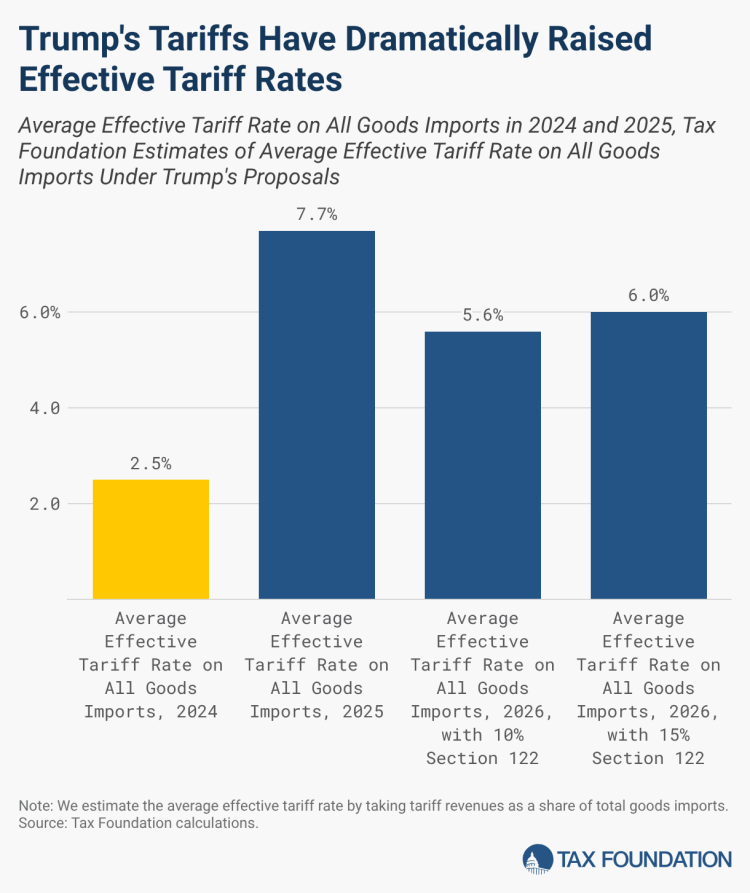

- The average effective tariff rate, which reflects actual tariff revenue raised as a share of actual goods imports, was 7.7 percent in 2025, the highest rate since 1947. If the 10 percent Section 122 tariffs expire after 150 days, we estimate the average effective tariff rate will be 5.6 percent in 2026—the highest since 1972.

- With the IEEPA being ruled illegal, we estimate that the remaining Section 232 tariffs imposed in 2025 and the 10 percent Section 122 tariffs will raise $668 billion in revenue from 2026-2035 on a conventional basis. The permanent Section 232 tariffs will reduce US GDP by 0.2 percent, before foreign retaliation. Accounting for negative economic effects, the revenue raised by the tariffs falls to $515 billion over the next decade. We estimate that the Section 232 tariffs raised $36 billion in net tax revenue in 2025.

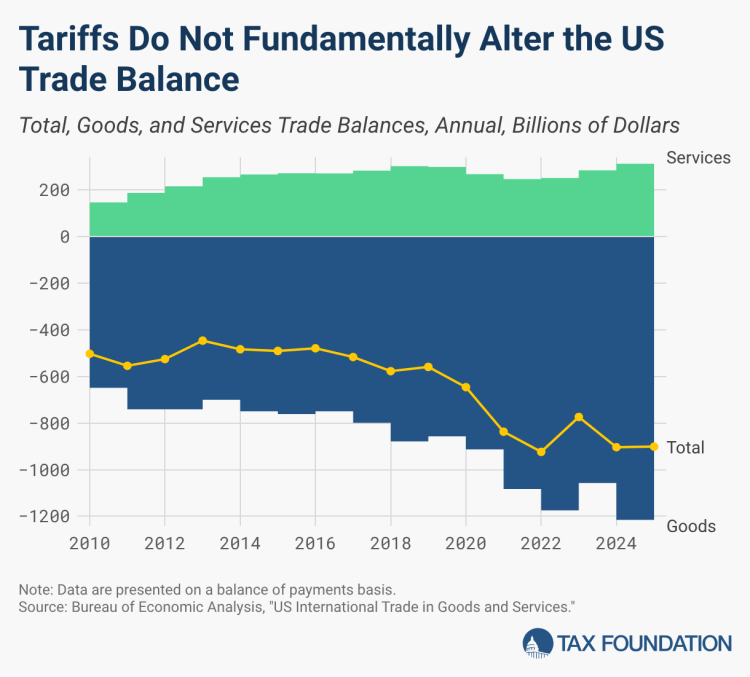

- The tariffs have not meaningfully altered the trade balance. The total trade deficit fell by only $2.1 billion in 2025, driven by an increase in the trade surplus of services.

- Historical evidence and recent studies show that tariffs are taxes that raise prices and reduce available quantities of goods and services for US businesses and consumers, resulting in lower income, reduced employment, and lower economic output.

Average Tariff Rates

The new tariffs will significantly raise the tariff rates the US applies to most imports.

According to the World Bank, the weighted average applied tariff was 1.5 percent in 2022. Prior to the ruling to strike down the International Emergency Economic Powers Act (IEEPA) tariffs, we estimate US imports faced a weighted-average applied tariff rate of 13.8 percent. While the 10 percent Section 122 tariffs are in effect, we estimate the applied rate will be 10.2 percent (at 15 percent, it would be 12.1 percent), and that it will fall to 6.7 percent after the Section 122 tariffs expire. The weighted average applied tariff rate measures the statutory tax rate imposed on different products from different countries, and it differs from averages measured by actual tariff revenues as a share of total goods imports.

We estimate the average effective tariff rate by taking tariff revenues as a share of total goods imports. In 2025, before the Supreme Court ruled the IEEPA tariffs illegal, the actual average effective tariff rate rose from 2.4 percent in 2024 to 7.7 percent, the highest since 1947. If the 10 percent Section 122 tariffs end after 150 days, we estimate the average effective tariff rate for 2026 will be 5.6 percent—the highest since 1972. (At 15 percent, it would be 6.0 percent and the highest since 1971.)

Tariff Revenue Collections

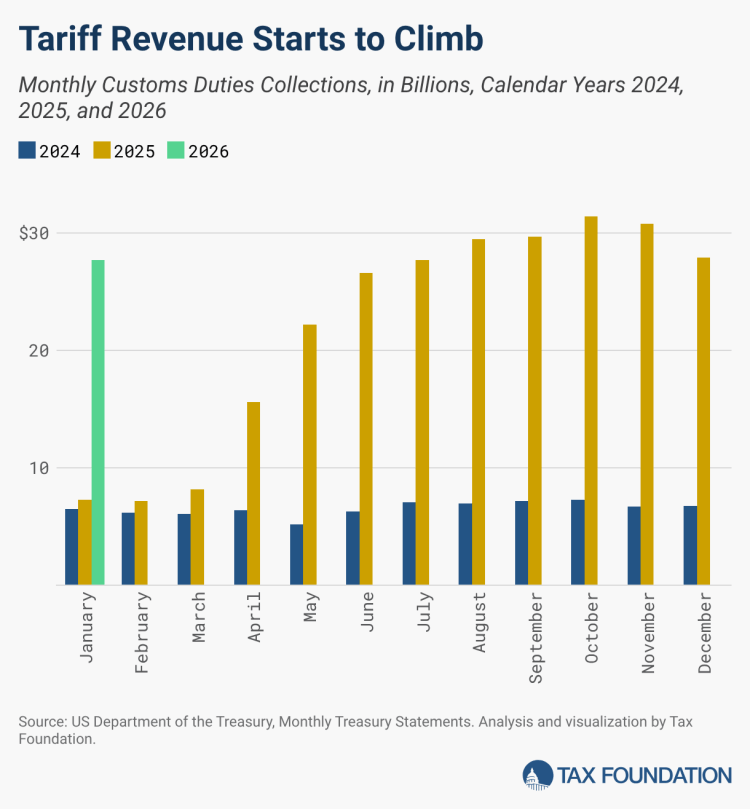

In calendar year 2025, customs duties raised $264 billion for the federal government, compared to $79 billion in calendar year 2024. Total customs duties revenues count new tariffs as well as pre-existing tariffs, such as those President Trump imposed in his first term. With the IEEPA tariffs being ruled illegal, the revenue collected by the government related to those tariffs will have to be refunded. The total revenue raised by tariffs will be less than the direct collections, because tariffs mechanically reduce the bases of income and payroll taxes. We estimate the government netted $36 billion from the new Section 232 tariffs in 2025.

The Balance of Trade

One of President Trump’s stated goals of imposing tariffs is to shrink the US trade deficit. However, a country’s balance of trade is not solely driven by trade policy, but instead, reflects broader macroeconomic balances between saving and investment and net lending and borrowing with the rest of the world.

In the United States, domestic investment outpaces domestic saving, requiring a capital inflow from the rest of the world to close the gap. The capital inflow represents net lending to the United States from the rest of the world to finance business investment as well as the government’s budget deficit. Because tariffs do not directly change the balance between domestic saving and investment, tariffs cannot permanently change the trade balance.

The last time the United States ran a trade surplus was in 1975; every year since, the United States has run a trade deficit. That the United States has consistently run trade deficits for decades is not an imminent economic problem. Net imports, another term for a trade deficit, can reflect the strength of the US economy in attracting foreign investment and in serving as a safe, reliable haven for foreign capital. When net imports finance the capital stock, it allows the US to enjoy a higher level of productivity and growth than otherwise would occur.

In 2025, the trade deficit fell by just $2.1 billion compared to 2024. The reduction in the trade deficit was due to an increase in the trade surplus of services, as the goods deficit actually increased by $25.5 billion year over year.

Economic Effects

On May 28, 2025, a panel of judges at the US International Court of Trade unanimously ruled that the IEEPA tariffs were illegal, a decision that was upheld by the US Court of Appeals. On February 20,2026, the Supreme Court ruled in a 6-3 decision in Learning Resources Inc. v. Trump and V.O.S. Selections v. United States that “IEEPA does not authorize the President to impose tariffs.” Our estimates below separate the effects of the IEEPA tariffs from the Section 232 tariffs, which were not affected by the ruling. See the Appendix for a detailed explanation of the modeled provisions.

We estimate that before accounting for any foreign retaliation, the Section 232 tariffs will reduce long-run US GDP by 0.2 percent. The Section 122 tariff expires after 150 days and thus would have no long-run economic impact. The IEEPA tariffs, including the scheduled “reciprocal” tariffs, would have reduced long-run GDP by an additional 0.3 percent.

As of September 1, 2025, threatened and imposed retaliatory tariffs affect $223 billion of US exports based on 2024 US import values; if fully imposed, we estimate they will reduce long-run US GDP by 0.2 percent.

Table 1. Estimated Economic Impact of 2025 Trump Tariffs

Source: Tax Foundation General Equilibrium Model, February 2026

Revenue Impacts

If imposed on a permanent basis, the tariffs will increase tax revenue for the federal government. We model the imposed tariffs together, accounting for interactions between the different rounds of tariffs and timing of implementation. Additionally, we account for income and payroll tax offsets, as tariffs mechanically reduce those tax bases. For this reason, the total tax revenue raised on net will be less than the tariff revenue reported by Treasury. Revenue is even lower on a dynamic basis, a reflection of the negative effect tariffs have on US economic output, reducing incomes and resulting tax revenues. Revenue would fall more when factoring in foreign retaliation, as retaliation would cause US output and incomes to shrink further.

On a conventional basis, before incorporating negative economic effects, we estimate that the Section 232 tariffs will increase US federal tax revenue by $635 billion from 2026 through 2035. The temporary 10 percent Section 122 tariffs will raise $25 billion in 2026 ($33 billion if 15 percent), replacing nearly 52 percent (or nearly 70 percent, if levied at 15 percent) of the revenue raised by IEEPA over 150 days. The IEEPA tariffs would have raised an additional $1.4 trillion in revenue over the next decade. The IEEPA tariffs raised less in 2025 than they were projected to in later years because they were not in effect for the full calendar year.

On a dynamic basis, incorporating the negative effects of the US-imposed tariffs on the US economy, we estimate that the Section 232 and temporary Section 122 tariffs will raise $515 billion from 2026 through 2035, about $145 billion less than the conventional estimate. The IEEPA tariffs would have raised an additional $1.1 trillion over the next decade, about $264 billion less than the conventional estimate. Incorporating the negative effects of imposed retaliatory tariffs as of September 1, 2025, further reduces 10-year revenue by $136 billion.

Table 2. Conventional Revenue Effects of 2025 Trump Tariffs

Table 3. Dynamic Revenue Effects of President Trump’s Tariffs

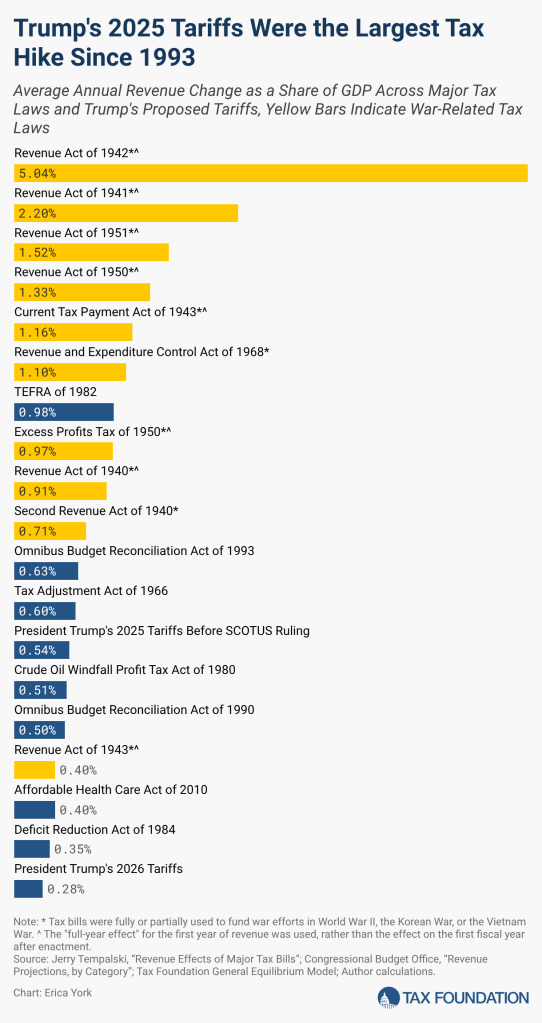

In 2026, the Trump tariffs including IEEPA would have increased federal tax revenues by $171.1 billion, or 0.54 percent of GDP, making the tariffs the largest tax hike since 1993. With the IEEPA tariff being ruled illegal, we estimate that the Section 232 tariffs and 10 percent Section 122 tariffs will increase federal tax revenues by $79 billion in 2026, or 0.25 percent of GDP, ranking as the 20th largest tax increase since 1940. (At 15 percent, the combined new tariffs would raise $87 billion in 2026, or 0.28 percent of GDP, and rank as the 18th largest tax increase since 1940.)

Distributional Impacts

In 2026, the tariffs will reduce after-tax incomes for all income groups. The top 1 percent will see a smaller reduction in after-tax income compared to others. Per US household, the tariffs altogether will amount to an average tax increase of $1,000 in 2025 and would have been a $1,300 average tax increase in 2026. However, with the IEEPA tariffs being ruled illegal, the tax increases will be smaller at $400 in 2026 for the Section 232 tariffs. The 10 percent Section 122 tariffs would increase the tax burden to $600. Notably, these averages do not capture additional costs to US households stemming from higher-priced alternative goods and loss of consumer choice.

Table 4. Distributional Effects of 2025 Trump Tariffs

|

|

Percent Change in After-Tax Income under Imposed Tariffs, 2026

|

Nominal Tax Change, 2026

|

||||

|---|---|---|---|---|---|---|

| Market Income Percentile | Section 232 Tariffs | IEEPA Tariffs | Combined | Section 232 Tariffs | IEEPA Tariffs | Combined |

| 0% – 20.0% | -0.3% | -0.8% | -1.1% | $36 | $79 | $115 |

| 20.0% – 40.0% | -0.3% | -0.8% | -1.1% | $99 | $215 | $314 |

| 40.0% – 60.0% | -0.4% | -0.8% | -1.1% | $192 | $418 | $610 |

| 60.0% – 80.0% | -0.3% | -0.8% | -1.1% | $339 | $740 | $1,079 |

| 80.0% – 100% | -0.3% | -0.7% | -1.0% | $927 | $2,019 | $2,946 |

| 80.0% – 90.0% | -0.4% | -0.8% | -1.1% | $540 | $1,177 | $1,717 |

| 90.0% – 95.0% | -0.4% | -0.8% | -1.1% | $756 | $1,647 | $2,404 |

| 95.0% – 99.0% | -0.3% | -0.7% | -1.1% | $1,258 | $2,742 | $4,000 |

| 99.0% – 99.9% | -0.3% | -0.7% | -1.0% | $3,014 | $6,566 | $9,580 |

| 99.9% – 100% | -0.2% | -0.5% | -0.8% | $15,987 | $34,830 | $50,818 |

Source: Tax Foundation General Equilibrium Model, February 2026

2025 Trade War Timeline & Current US Tariff Policy

President Trump signed an executive order on January 20, 2025, instructing certain cabinet secretaries to develop reports on trade practices and recommendations for tariffs due by April 1, 2025. Since then, several new tariffs and tariff investigations have been threatened, initiated, and/or imposed, and at least five court cases have challenged the legality of the tariff executive order. No court yet has ruled in favor of the unlimited emergency tariff authority Trump claimed, although his administration has been quick to appeal these rulings.

Table 5. IEEPA Reciprocal Tariff Rates and Affected Imports

Note: These tariffs were overturned by the Supreme Court on Februrary 20, 2026

Source: US International Trade Commission “Imports for Consumption”; Federal Register; Tax Foundation calculations

Country-Specific Tariffs

- IEEPA Border Security and Fentanyl Tariffs: President Trump signed three executive orders on February 1, 2025, to impose 25 percent tariffs on Canada and Mexico and 10 percent tariffs on China using International Emergency Economic Powers Act (IEEPA) authority, to go into effect on February 4. On February 20, 2026, the Supreme Court ruled that the President cannot use IEEPA to impose tariffs.

- China: The 10 percent tariffs on all imports from China took effect on February 4, 2025. On February 27, Trump said the tariffs on China would increase by another 10 percent beginning March 4, which has taken effect. On June 11, Trump announced a trade deal with China that would leave in place the current 20 percent “fentanyl” and 10 percent “reciprocal” tariffs (for a total of 30 percent), pausing higher tariffs for 60 days. On August 11, President Trump announced that the increase in the reciprocal tariff to 125 percent would be paused for another 90 days. On October 10, the president announced he would impose an additional 100 percent tariff on China starting November 1, as a response to China’s imposition of export controls on rare earth minerals. On October 26, a “framework” of a deal with China was achieved, averting the implementation of an additional 100 percent tariff. On October 30, the president announced that the IEEPA “fentanyl” tariff on China would be lowered to 10 percent. As of December 1, because the IEEPA tariffs stack on top of the existing Section 301 tariffs on certain imports from China, some goods face tariffs as high as 45 percent.

- Canada: The tariffs on Canada received a 30-day suspension and took effect March 4. On March 5, the president exempted auto imports from the tariffs until April 2, and on March 6, the president exempted imports covered by the USMCA trade deal (approximately 38 percent of imports from Canada in 2024) until April 2 while lowering the tariff on non-USMCA potash (a fertilizer used in farming) and certain energy imports to 10 percent. On April 2, the exemption was extended indefinitely. On March 11, the president said the 25 percent rate on steel and aluminum would double to 50 percent in response to Canada’s retaliation, but later in the day walked back the doubling. On July 10, President Trump threatened Canada with a 35 percent tariff that would take effect August 1. On August 1, the 35 percent tariff on Canada went into effect. On October 25, President Trump announced he would be imposing an additional 10 percent tariff on Canadian imports, though no effective date was given. On January 31, 2026, President Trump threatened to increase tariffs on Canada to 50 percent and impose additional tariffs on its aircrafts if it pursued a trade deal with China.

- Mexico: The tariffs on Mexico received a 30-day suspension and took effect on March 4. On March 5, the president exempted auto imports from the tariffs until April 2, and on March 6 the president exempted imports covered by the USMCA trade deal (approximately 49 percent of imports from Mexico in 2024) until April 2. On April 2, the exemption was extended indefinitely. On July 12, President Trump announced the reciprocal tariffs for Mexico would increase to 30 percent by August 1. On July 31, he announced the tariff increase on Mexico would be delayed for 90 days. On October 28, President Trump announced he would be pausing the tariff increase indefinitely.

- IEEPA “Reciprocal” Tariffs: President Trump signed a presidential memorandum on February 13, 2025, to develop a plan for increasing US tariffs in response to other countries’ tariffs, tax policies, and any other policies including exchange rates and unfair practices. The recommendations are due April 1, 2025, and the president has indicated they will begin taking effect on April 2. The so-called reciprocal tariffs are applied to imports from nearly every US trading partner, but do not include goods that face product-specific tariffs like steel, aluminum, autos, and auto parts, and they also exclude a specific list of energy-related and other goods. On February 20, 2026, the Supreme Court ruled that the President cannot use IEEPA to impose tariffs.

-

- On April 2, 2025, the president announced a universal tariff of 10 percent, with higher tariffs on trading partners, as high as 50 percent, depending on their trade balance with the United States.

- On April 7, 2025, in response to China’s retaliation, President Trump indicated another 50 percent tariff would apply to China beginning April 9, which was increased on April 9 to a total rate of 125 percent under the reciprocal tariffs. The rate on most imports from China is 145 percent when accounting for the IEEPA border security and fentanyl tariffs.

- The 10 percent universal tariff took effect April 5, 2025, and on April 9, 2025, President Trump announced a 90-day pause on the reciprocal tariffs for all other countries excluding China.

- On May 8, 2025, the president announced the outlines of a trade deal with the UK, which would maintain the 10 percent “reciprocal” tariff, but lower the 25 percent auto tariff to 10 percent on the first 100,000 vehicle imports and eliminate the 25 percent steel and aluminum tariffs. In 2024, the US imported about 180,000 autos worth $10.5 billion and $1.8 billion of steel and aluminum from the UK. On June 30, 2025, the US-UK deal went into effect. The 25% tariff on imports of UK steel and aluminum will remain in place.

- On May 12, 2025,the Treasury Secretary announced a 90-day pause on escalations with China, reducing the 125 percent tariff to 10 percent. The China reciprocal tariffs were scheduled to go into effect August 12, 2025.

- On May 28, 2025, a panel of judges at the US International Court of Trade unanimously ruled that the IEEPA tariffs were illegal. The Trump administration immediately filed an appeal. The ruling provided the president up to 10 days to begin the process of halting collections of the IEEPA tariffs. The ruling would not apply to the Section 232 and 301 tariffs that are currently in place. Importers that paid tariffs under the IEEPA would be eligible for retroactive relief.

- On May 29, 2025, a second federal court ruled against the IEEPA tariffs.

- On June 10, 2025, the US Court of Appeals for the Federal Circuit of Washington, DC decided to allow Trump’s IEEPA tariffs to remain in effect until the court rules to uphold or reject the lower court’s decision, with arguments scheduled for July 31, 2025.

- On July 2, 2025, the president announced that the US had reached a deal with Vietnam. A 20 percent baseline tariff would remain on imports from Vietnam, while a 40 percent tariff would be imposed on any transshipments. No effective date has been scheduled for the deal.

- On July 7, 2025, the president announced that the reciprocal tariffs would be delayed until August 1. He sent letters to 14 countries, including Japan and South Korea, indicating the tariffs they would face if they did not present a trade deal with the US by the end of July. He also threatened “BRICS-aligned countries” with an additional 10 percent tariff.

- On July 9, 2025, Trump’s administration sent letters to 7 more countries and threatened Brazil with a 50 percent tariff that would take effect August 1, 2025.

- On July 14, 2025, President Trump threatened Russia with 100 percent tariffs.

- On July 22, 2025, President Trump announced that the US had reached a deal with the Philippines and Indonesia that would set their reciprocal tariff rates at 19 percent, down from the proposed 20 percent and 32 percent respectively.

- On July 23, 2025, President Trump announced that the US had reached a deal with Japan that would set its reciprocal tariff rate at 15 percent, down from the proposed 24 percent.

- On July 30, 2025, President Trump signed an executive order imposing an additional 40 percent tariff on Brazil, delaying implementation of the tariff until August 6, 2025, and published a list of exemptions. He also signed an executive order that would end the de minimis exemption for all countries starting August 29, 2025.

- On July 31, 2025, President Trump signed an executive order with changes to reciprocal tariff rates on more than 60 countries and additional penalties for transshipments, delaying implementation of those until August 7, 2025.

- On August 6, 2025, the president announced he would double the reciprocal tariff rate on India to 50 percent, effective August 27, 2025, as a “penalty” for their Russian oil purchases.

- On August 7, 2025, the reciprocal tariff increases took effect.

- On August 29, 2025, the US Court of Appeals declared the IEEPA tariffs illegal, ruling that the president lacked the authority to impose them under his emergency powers. The tariffs will remain in effect while the administration prepares its appeal to the Supreme Court. The Supreme Court will hear oral arguments on November 5, 2025.

- On September 5, 2025, the president updated the exemptions list to include an additional $30 billion worth of goods (based on 2024 values), and removed another $6 billion worth of goods from the exemptions list, subjecting those to the IEEPA tariffs.

- On October 26, 2025, President Trump announced a new trade deal with Cambodia and released a list of goods that would be exempt from its reciprocal tariff.

- On November 14, 2025, President Trump released a new exemptions list excluding certain food and agricultural products from the IEEPA tariffs, except for Brazil, covering about $51.5 billion worth of imports based on 2024 import levels. The president also lowered Switzerland’s reciprocal tariff rate from 39 percent to 15 percent.

- On November 21, 2025, President Trump released an additional agricultural exemptions list for Brazil.

- On January 15, 2026, President Trump announced a new trade deal with Taiwan that would lower its reciprocal tariff rate from 20 percent to 15 percent.

- On February 2, 2026, President Trump announced that he would drop the 25 percent tariff on India for purchasing Russian oil, and would lower its reciprocal tariff from 25 percent to 18 percent.

-

- Section 122 Tariffs: On February 20, 2026, President Trump signed an executive order that would impose a 10 percent tariff on all countries, with various exemptions, under Section 122 in response to “large and serious United States balance-of-payments deficits.” We estimate that the tariffs would apply to about $1.2 trillion worth of imports, accounting for all exemptions including those covered under Section 232 and the USMCA. The tariff will expire after 150 days. On February 21, 2026, the president increased the tariff rate to 15 percent.

- Venezuelan Oil Tariffs: President Trump signed an executive order on March 24, 2025, to impose an additional 25 percent tariff on Venezuela and any countries that purchase oil and gas from Venezuela, which could become effective April 2, 2025.

- European Union: President Trump announced plans on February 26, 2025, to impose tariffs of 25 percent on imports from the European Union. The authority to impose these tariffs has not been specified. On April 2, 2025, President Trump specified the “reciprocal” tariff rate on imports from the EU would be 20 percent. On May 23, 2025, President Trump announced he would be imposing a 50 percent reciprocal tariff on the EU beginning June 1, 2025. On May 25, 2025, he announced these tariffs would take effect July 9, 2025, instead. On July 12, 2025, President Trump announced the reciprocal tariffs for the EU would be set at 30 percent by August 1, 2025. This is down from the previous reciprocal tariff for the EU announced in May 2025, which had been set at 50 percent. On July 27, 2025, President Trump announced that the US had reached a deal with the EU that would set its reciprocal tariff rate at 15 percent, down from the proposed 30 percent. On August 21, 2025, President Trump announced as part of the EU deal that he would reduce the tariff on EU autos from 27.5 percent to 15 percent, conditional on the EU introducing legislation to lower its tariffs on certain US goods. He also announced that any new tariffs on pharmaceuticals and semiconductors would be capped at 15 percent for the EU. On September 26, 2025, the president released an updated list of EU exemptions.

- Tariff Stacking: On April 29, 2025, the president signed an executive order to prevent certain tariffs from stacking; rather than add on, the executive order specifies a hierarchy for which tariffs apply. The top priority is auto tariffs, followed by IEEPA “fentanyl” tariffs on Canada and Mexico, followed by steel and aluminum tariffs.

- Russian Oil Tariffs: On August 6, 2025, President Trump announced an executive order to impose tariffs on any countries importing oil from Russia, applying to imports from India at a 25 percent tariff rate. On February 2, 2026, President Trump announced he would lift the 25 percent tariffs on India.

- Iranian Oil Tariffs: On January 12, 2026, President Trump announced that countries that buy Iranian oil would face an additional 25 percent tariff.

- Greenland Tariffs: On January 17, 2026, President Trump announced that he would impose an additional 10 percent tariff on Denmark, Norway, Sweden, France, Germany, the United Kingdom, the Netherlands, and Finland, starting February 1, 2026. The tariffs will rise to 25 percent on June 1, 2026, if the US is not able to acquire Greenland by then. On January 21, 2026, the president announced he would not be imposing these tariffs.

Product-Specific Tariffs

- Semiconductors: President Trump said on January 27, 2025, he would announce new tariffs on computer chips, semiconductors, and pharmaceuticals. On February 18 he announced the rates on semiconductors and pharmaceuticals would be “25 percent and higher.” The Department of Commerce initiated a Section 232 investigation on April 1, 2025. On January 14, 2026, the president issued a proclamation detailing a new 25 percent tariff on a narrow category of specific chips that are then re-exported beginning January 15, 2026. The proclamation noted that when negotiations with trading partners conclude, broader tariffs at significant rates could be imposed.

- Pharmaceuticals: On July 8, 2025, the president threatened a 200 percent tariff on pharmaceuticals. On August 6, 2025, he indicated the semiconductor tariffs would be 100 percent and the pharmaceutical tariffs would go as high as 250 percent. The president announced on September 26, 2025, that he would be imposing a 100 percent tariff on pharmaceuticals on October 1, 2025, although no proclamation has been issued yet. Tariffs would be capped at 15 percent for the EU and Japan. Generics would be exempt.

- Steel and Aluminum: President Trump signed two proclamations on February 10, 2025, to expand the existing Section 232 tariffs on steel and aluminum. The orders end all existing exemptions for the tariffs, expand the list of derivative articles, and raise the tariff rate on aluminum from 10 percent to 25 percent. The changes took effect March 12, 2025. On May 30, 2025, President Trump announced the steel and aluminum tariffs would double to 50 percent beginning on June 4, 2025 for all countries except the UK. On June 13, 2025, the Trump administration announced an expansion to apply the tariffs to the steel content of eight more product lines effective June 23, 2025, including dishwashers, refrigerators, washing machines, dryers, freezers, stoves, ovens, and food waste disposals. On August 19, 2025, President Trump added new steel and aluminum derivatives to the annex that would face the 50 percent tariffs.

- Autos: President Trump announced on February 14, 2025, that he plans to impose tariffs on auto imports beginning on April 2, 2025. He said on February 18 the rate on autos would be “in the neighborhood of 25 percent” while the rates on semiconductors and pharmaceuticals would be “25 percent and higher.” On March 26, 2025, Trump signed a proclamation authorizing 25 percent tariffs on autos and certain auto parts under Section 232 to take effect April 3, 2025, for autos and before May 3, 2025 for auto parts. US-based content of certain imports from Canada and Mexico will be exempt. As part of US-UK deal, auto imports up to 100,000 would face a 10 percent tariff, while any imports beyond that quota would be subject to a 25 percent tariff. As part of the US-Japan deal, the rate on auto imports from Japan fell to 15 percent effective September 16, 2025.

- Heavy Trucks and Buses: On April 22, 2025, President Trump issued a Section 232 investigation into medium and heavy-duty trucks and parts, including buses. The report is due January 16, 2026. On September 30, 2025, the president announced that he would be imposing 25 percent tariffs on these trucks and a 10 percent on buses effective October 1, 2025, although he later changed the effective date to November 1, 2025. Tariffs would be capped at 15 percent for the EU.

- Copper: President Trump directed the Commerce Department on February 25, 2025, to begin a Section 232 national security investigation for copper imports; the findings of the report are due by November 22, 2025. On July 8, 2025, he announced he would be imposing a 50 percent tariff on copper on August 1, 2025. On August 1, 2025, the copper tariffs went into effect, though raw materials were exempted.

- Lumber: President Trump directed the Commerce Department on March 1, 2025, to begin a Section 232 national security investigation into timber, lumber, and derivative imports; the findings of the report are due by November 26, 2025. On September 30, 2025, the president issued a proclamation announcing that he would be imposing 10 percent tariffs on lumber effective October 14, 2025.

- Processed Critical Minerals: On April 22, 2025, the Department of Commerce initiated a Section 232 investigation into processed critical minerals. On January 14, 2026, the president issued a proclamation to continue negotiations with trading partners to secure adequate supplies of critical minerals. No new tariffs have yet been planned, however, the proclamation also suggests that tariffs or minimum import prices could be considered in the future.

- Wind Turbines: On August 13, 2025, the Department of Commerce initiated a Section 232 investigation into wind turbines.

- Furniture: On August 22, 2025, President Trump announced that he planned to impose higher tariffs on furniture. On September 30, 2025, the president issued a proclamation announcing that he would be imposing tariffs on kitchen cabinets, bathroom vanities, and upholstered furniture of 25 percent, effective October 14, 2025. The rates on upholstered furniture would increase to 30 percent on January 1, 2026, and the rates on kitchen cabinets and bathroom vanities would increase to 50 percent on that date. On December 31, 2025, the president paused the tariff increases until January 1, 2027. Tariffs on these products are capped at 10 percent for the UK and 15 percent for the EU and Japan.

- Agricultural Products: President Trump posted on March 3, 2025, that tariffs on “external” agricultural products would begin April 2, 2025.

- Apple: President Trump announced on May 23, 2025 that Apple would face additional 25 percent tariffs if it did not source its iPhone components from the US.

- Maritime Taxes: On April 9, 2025, President Trump signed an executive order that would impose Section 301 fees on deliveries by Chinese ships. China threatened to retaliate. The fees are scheduled to take effect October 14, 2025, starting at $50 per net ton for the arriving vessel. On October 30, 2025, President Trump and China agreed to suspend these port fees on each other’s ships for a year.

- Export Tariffs: On August 11, 2025, President Trump announced that he had negotiated a deal with Nvidia and AMD that would allow them to sell certain semiconductor chips to China in exchange for the US government receiving 15 percent of the generated revenue. It appears that rather than impose an export tariff (which is constitutionally prohibited), the Section 232 tariff that took effect in January 2026 will be used instead, applying only to certain semiconductor imports that are then re-exported.

- Foreign Films: On September 30, 2025, President Trump announced that he intends to impose 100 percent tariffs on films that are not made in the US, although it is unclear how this would be enforced.

Retaliation

- China

-

- IEEPA fentanyl retaliation: 10 percent and 15 percent tariffs on $13.9 billion of US exports (including ag equipment and oil) effective on February 10, 2025; 10 percent and 15 percent tariffs on $19.5 billion of US exports (including agricultural products) effective on March 10, 2025.

- IEEPA universal retaliation: 34 percent tariffs on all $144 billion of US exports announced on April 4, 2025; on April 9, 2025, China increased its retaliation to 84 percent on all US exports; on April 11, 2025, China increased its retaliation to 125 percent on all US exports; on May 12, 2025, China reduced its retaliation to 10 percent on all US exports under a 90-day pause.

- As part of the trade deal announced June 10, 2025, China paused tariff increases for 90 days and walked back some of its export restrictions, including for rare earth minerals and magnets.

- On October 9, 2025, China announced additional export controls on rare earth minerals that would take effect November 8, 2025. The US and China later that month agreed to a “framework” of a deal that would avert the implementation of these export controls.

-

- Canada

-

- IEEPA fentanyl retaliation: 25 percent tariffs on $20.8 billion of US exports effective on March 4, 2025; 25 percent tariffs on $86.7 billion of US exports scheduled for March 23, 2025; planned 25 percent tax on electricity exports from Ontario to the US, currently suspended

- Section 232 steel and aluminum retaliation: 25 percent tariffs on $20.7 billion of US exports effective March 13, 2025

- Section 232 auto retaliation: 25 percent tariffs on $30.5 billion of US autos

- On August 22, 2025, Prime Minister Mark Carney announced he would remove retaliatory tariffs on US exports except for autos, steel, and aluminum, effective September 1, 2025.

-

- European Union

-

- Section 232 retaliation: Lift suspension of previous tariffs, with rates of up to 50 percent, affecting $8 billion of US exports scheduled for April 1, 2025 (including whiskey); expand tariffs to an additional $20 billion of US exports scheduled for April 13, 2025. On July 15, 2025, the EU released a list of $84 billion worth of US goods that would face retaliatory tariffs if no deal is reached by August 1, 2025. On August 4, 2025, the retaliatory tariffs were delayed for six months.

-

Modeling Notes

Methodological Note: On October 23, 2025, we refined how we apply our elasticity estimates to tariffs. We adopted a functional form equation and a higher elasticity of -2 to reflect nonlinearity across different tariff rates. These refinements are based on research from Boehm et al. and the USITC. The implication of this methodological change is that higher tariff rates cause imports to drop significantly but not fall all the way to zero. As a result, some of our tariff revenue estimates, including for the 100 percent tariffs on China, are higher than previously estimated.

We updated our income and payroll tax offset to reflect the new values under the One Big Beautiful Bill Act (OBBBA), and it averages .238 from 2026 through 2035.

President Trump has imposed and threatened a variety of tariffs. Based on 2024 import values, the tariffs affect approximately $2.2 trillion of US goods imports (excluding de minimis), or 67 percent of US goods imports. However, if the IEEPA tariffs are permanently enjoined, the remaining new tariffs will affect more than $600 billion, or 20 percent, of goods imports. We model the following policies:

- A 20 percent tariff on all imports from China, lowered to 10 percent effective November 1, 2025 plus a 10 percent baseline tariff on all imports from China effective April 2, excluding those subject to Section 232 tariffs or on the exclusion list (resulting in a 20 percent tariff on most imports from China).

- A 25 percent tariff on all imports from Mexico in 2025. USMCA-compliant imports are exempt from the tariffs indefinitely. With an increase in USMCA-compliant goods coming through the border, we estimate that tariffs will apply to $38 billion of Mexican imports in our baseline on an annualized basis.

- A 10 percent tariff on energy and potash imports indefinitely, plus a 25 percent tariff on all remaining imports from Canada in 2025 until August 1,2025, when the rate increases to 35 percent. USMCA-compliant imports are exempt from the tariffs indefinitely. With an increase in USMCA-compliant goods coming through the border, we estimate that tariffs will apply to $42billion of Canadian imports in our baseline on an annualized basis.

- A 10 percent baseline tariff on all countries from April through June of 2025, exempting Section 232 goods, Annex II goods, and specified electronics.

- A range of “reciprocal” tariffs on most US trading partners, exempting Section 232 goods, Annex II goods, and other specified country exemptions. We do not model the additional penalties for transshipments announced on July 31,2025. Excluding the EU, China, Canada, and Mexico, the so-called reciprocal tariffs on the rest of the world result in a trade-weighted average tariff rate of 17 percent.

- Expansions to the Section 232 steel and aluminum tariffs, including ending country exemptions, raising the rate to 50 percent except for imports from the UK which remain at 25 percent, and expanding steel and aluminum products covered. We do not model the expanded derivatives list due to data limitations.

-

- Increasing the covered products, excluding expanded derivatives due to data limitations, increase imports subject to the tariffs by another $47 billion.

- A 25 percent tariff on all autos and certain auto parts, excluding US content of imports from Canada and Mexico, and providing a lower rate on auto imports from the UK, Japan, and South Korea. We illustrate the effects of this policy with 25 percent tariffs on all auto and auto parts specified in the Federal Register excluding USMCA trade.

- A 50 percent tariff on copper imports excluding raw materials and derivatives.

- A 10 percent tariff on lumber.

- A 25 percent tariff on upholstered furniture effective October 14, 2025, increasing to 30 percent on January 1, 2027 (10 percent for the UK and 15 percent for the EU, Japan, and South Korea).

- A 25 percent tariff on bathroom vanities and kitchen cabinets effective October 14, 2025, increasing to 50 percent January 1, 2027 (10 percent for the UK and 15 percent for the EU, Japan, and South Korea).

-

- Retaliation effective as of September 1, 2025, excluding export controls.

- Ending the exemption for de minimis imports.

- China

Historical Evidence

Tariffs Raise Prices and Reduce Economic Growth

Economists generally agree free trade increases the level of economic output and income, while conversely, trade barriers reduce economic output and income. Historical evidence shows tariffs raise prices and reduce available quantities of goods and services for US businesses and consumers, resulting in lower income, reduced employment, and lower economic output.

Tariffs could reduce US output through a few channels. One possibility is a tariff may be passed on to producers and consumers in the form of higher prices. Tariffs can raise the cost of parts and materials, which would raise the price of goods using those inputs and reduce private sector output. This would result in lower incomes for both owners of capital and workers. Similarly, higher consumer prices due to tariffs would reduce the after-tax value of both labor and capital income. Because higher prices would reduce the return to labor and capital, they would incentivize Americans to work and invest less, leading to lower output.

Alternatively, the US dollar may appreciate in response to tariffs, offsetting the potential price increase for US consumers. The more valuable dollar, however, would make it more difficult for exporters to sell their goods on the global market, resulting in lower revenues for exporters. This would also result in lower US output and incomes for both workers and owners of capital, reducing incentives for work and investment and leading to a smaller economy.

Many economists have evaluated the consequences of the trade war tariffs on the American economy, with results suggesting the tariffs have raised prices and lowered economic output and employment since the start of the trade war in 2018.

- A February 2018 analysis by economists Kadee Russ and Lydia Cox found that steel‐consuming jobs outnumber steel‐producing jobs 80 to 1, indicating greater job losses from steel tariffs than job gains.

- A March 2018 Chicago Booth survey of 43 economic experts revealed that 0 percent thought a US tariff on steel and aluminum would improve Americans’ welfare.

- An August 2018 analysis from economists at the Federal Reserve Bank of New York warned the Trump administration’s intent to use tariffs to narrow the trade deficit would reduce imports and US exports, resulting in little to no change in the trade deficit.

- A March 2019 National Bureau of Economic Research study conducted by Pablo D. Fajgelbaum and others found that the trade war tariffs did not lower the before-duties import prices of Chinese goods, resulting in US importers taking on the entire burden of import duties in the form of higher after-duty prices.

- An April 2019 University of Chicago study conducted by Aaron Flaaen, Ali Hortacsu, and Felix Tintelnot found that after the Trump administration imposed tariffs on washing machines, washer prices increased by $86 per unit and dryer prices increased by $92 per unit, due to package deals, ultimately resulting in an aggregate increase in consumer costs of over $1.5 billion.

- An April 2019 research publication from the International Monetary Fund used a range of general equilibrium models to estimate the effects of a 25 percent increase in tariffs on all trade between China and the US, and each model estimated that the higher tariffs would bring both countries significant economic losses.

- An October 2019 study by Alberto Cavallo and coauthors found tariffs on imports from China were almost fully passed through to US import prices but only partially to retail consumers, implying some businesses absorbed the higher tariffs, reducing retail margins, instead of passing them on to retail consumers.

- In December 2019, Federal Reserve economists Aaron Flaaen and Justin Pierce found a net decrease in manufacturing employment due to the tariffs, suggesting that the benefit of increased production in protected industries was outweighed by the consequences of rising input costs and retaliatory tariffs.

- A February 2020 paper from economists Kyle Handley, Fariha Kamal, and Ryan Monarch estimated the 2018–2019 import tariffs were equivalent to a 2 percent tariff on all US exports.

- A December 2021 review of the data and methods used to estimate the trade war effects through 2021, by Pablo Fajgelbaum and Amit Khandelwal, concluded that “US consumers of imported goods have borne the brunt of the tariffs through higher prices, and that the trade war has lowered aggregate real income in both the US and China, although not by large magnitudes relative to GDP.”

- A January 2022 study from the US Department of Agriculture estimated the direct export losses from the retaliatory tariffs totaled $27 billion from 2018 through the end of 2019.

- A May 2023 United States International Trade Commission report from Peter Herman and others found evidence for near complete pass-through of the steel, aluminum, and Chinese tariffs to US prices. It also found an estimated $2.8 billion production increase in industries protected by the steel and aluminum tariffs was met with a $3.4 billion production decrease in downstream industries affected by higher input prices.

- A January 2024 International Monetary Fund paper found that unexpected tariff shocks tend to reduce imports more than exports, leading to slight decreases in the trade deficit at the expense of persistent gross domestic product losses—for example, the study estimates reversing the 2018–2019 tariffs would increase US output by 4 percent over three years.

- A January 2024 study by David Autor and others concludes that the 2018–2019 tariffs failed to provide economic help to the heartland: import tariffs had “neither a sizable nor significant effect on US employment in regions with newly‐protected sectors” and foreign retaliation “by contrast had clear negative employment impacts, particularly in agriculture.”

Historical Context

2024 Campaign Proposals

Tariffs featured heavily in the 2024 presidential campaign as candidate Trump proposed a new 10 percent to 20 percent universal tariff on all imports, a 60 percent tariff on all imports from China, higher tariffs on EVs from China or across the board, 25 percent tariffs on Canada and Mexico, and 10 percent tariffs on China.

We estimate Trump’s proposed 20 percent universal tariffs and an additional 50 percent tariff on China to reach 60 percent will reduce long-run economic output by 1.3 percent before any foreign retaliation. They will increase federal tax revenues by $3.8 trillion ($3.1 trillion on a dynamic basis before retaliation) from 2025 through 2034.

2018-2019 Trade War: Economic Effects of Imposed and Retaliatory Tariffs

Using the Tax Foundation’s General Equilibrium Model, we estimate the Trump-Biden Section 301 and Section 232 tariffs will reduce long-run GDP by 0.2 percent, the capital stock by 0.1 percent, and hours worked by 142,000 full-time equivalent jobs. The reason tariffs have no impact on pre-tax wages in our estimates is that, in the long run, the capital stock shrinks in proportion to the reduction in hours worked, so that the capital-to-labor ratio, and thus the level of wages, remains unchanged. Removing the tariffs would boost GDP and employment, as Tax Foundation estimates have shown for the Section 232 steel and aluminum tariffs.

Table 6. Estimated Impact of US Imposed Tariffs, 2018-2019 Trade War

| GDP | -0.2% |

| Capital Stock | -0.1% |

| Pre-Tax Wages | 0.0% |

| Full-Time Equivalent (FTE) Jobs | -142,000 |

Note: 2018-2019 trade war tariffs reflect Section 301 tariffs on imports from China and Section 232 tariffs on certain steel and aluminum imports.

Source: Tax Foundation General Equilibrium Model, June 2024.

We estimate the retaliatory tariffs stemming from Section 232 and Section 301 actions total approximately $13.2 billion in tariff revenues. Retaliatory tariffs are imposed by foreign governments on their country’s importers. While they are not direct taxes on US exports, they raise the after-tax price of US goods in foreign jurisdictions, making them less competitively priced in foreign markets. We estimate the retaliatory tariffs will reduce US GDP and the capital stock by less than 0.05 percent and reduce full-time employment by 27,000 full-time equivalent jobs. Unlike the tariffs imposed by the United States, which raise federal revenue, tariffs imposed by foreign jurisdictions raise no revenue for the US but result in lower US output.

Table 7. Estimated Impact of US Retaliatory Tariffs, 2018-2019 Trade War

| GDP | Less than -0.05% |

| Capital Stock | Less than -0.05% |

| Pre-Tax Wages | 0.0% |

| Full-Time Equivalent (FTE) Jobs | -27,000 |

Note: 2018-2019 retaliation reflects retaliatory tariffs on $6 billion of US exports in response to Section 232 tariffs and more than $106 billion of US exports in response to Section 301 tariffs.

Source: Tax Foundation General Equilibrium Model, June 2024.

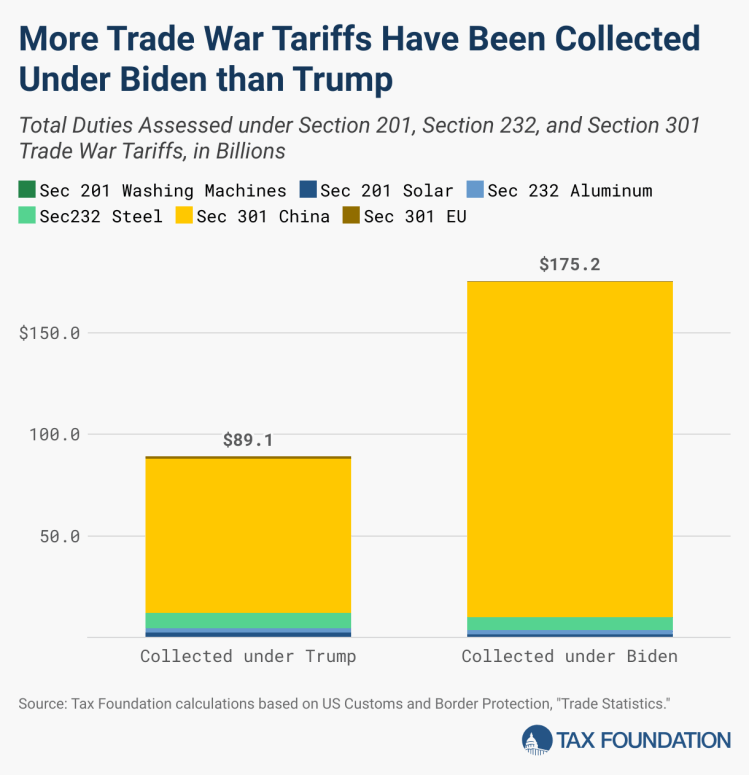

Tariff Revenue Collections Under the Trump-Biden Tariffs

As of the end of 2024, the trade war tariffs have generated more than $264 billion of higher customs duties collected for the US government from US importers. Of that total, $89 billion, or about 34 percent, was collected during the Trump administration, while the remaining $175 billion, or about 64 percent, was collected during the Biden administration.

Before accounting for behavioral effects, the $79 billion in higher tariffs amount to an average annual tax increase on US households of $625. Based on actual revenue collections data, trade war tariffs have directly increased tax collections by $200 to $300 annually per US household, on average. The actual cost to households is higher than both the $600 estimate before behavioral effects and the $200 to $300 after, because neither accounts for lower incomes as tariffs shrink output, nor the loss in consumer choice as people switch to alternatives that do not face tariffs.

2018-2019 Trade War Timeline

The Trump administration imposed several rounds of tariffs on steel, aluminum, washing machines, solar panels, and goods from China, affecting more than $380 billion worth of trade at the time of implementation and amounting to a tax increase of nearly $80 billion. The Biden administration maintained most tariffs, except for the suspension of certain tariffs on imports from the European Union, the replacement of tariffs with tariff-rate quotas (TRQs) on steel and aluminum from the European Union and United Kingdom and imports of steel from Japan, and the expiration of the tariffs on washing machines after a two-year extension. In May 2024, the Biden administration announced additional tariffs on $18 billion of Chinese goods for a tax increase of $3.6 billion.

Altogether, the trade war policies currently in place add up to $79 billion in tariffs based on trade levels at the time of tariff implementation. Note the total revenue generated will be less than our static estimate because tariffs reduce the volume of imports and are subject to evasion and avoidance (which directly lowers tariff revenues) and they reduce real income (which lowers other tax revenues).

Section 232, Steel and Aluminum

In March 2018, President Trump announced the administration would impose a 25 percent tariff on imported steel and a 10 percent tariff on imported aluminum. The value of imported steel totaled $29.4 billion, and the value of imported aluminum totaled $17.6 billion in 2018. Based on 2018 levels, the steel tariffs would have amounted to $9 billion and the aluminum tariffs to $1.8 billion. Several countries, however, have been excluded from the tariffs.

In early 2018, the US reached agreements to permanently exclude Australia from steel and aluminum tariffs, use quotas for steel imports from Brazil and South Korea, and use quotas for steel and aluminum imports from Argentina.

In May 2019, President Trump announced that the US was lifting tariffs on steel and aluminum from Canada and Mexico.

In 2020, President Trump expanded the scope of steel and aluminum tariffs to cover certain derivative products, totaling approximately $0.8 billion based on 2018 import levels.

In August 2020, President Trump announced that the US was reimposing tariffs on aluminum imports from Canada. The US imported approximately $2.5 billion worth of non-alloyed unwrought aluminum, resulting in a $0.25 billion tax increase. About a month later, the US eliminated the 10 percent tariff on Canadian aluminum that had just been reimposed.

In 2021 and 2022, the Biden administration reached deals to replace certain steel and aluminum tariffs with tariff rate quota systems, whereby certain levels of imports will not face tariffs, but imports above the thresholds will. TRQs for the European Union took effect on January 1, 2022; TRQs for Japan took effect on April 1, 2022; and TRQs for the UK took effect on June 1, 2022. Though the agreements on steel and aluminum tariffs will reduce the cost of tariffs paid by some US businesses, a quota system similarly leads to higher prices, and further, retaining tariffs at the margin continues the negative economic impact of the previous tariff policy.

Tariffs on steel, aluminum, and derivative goods currently account for $2.7 billion of the $79 billion in tariffs, based on initial import values. Current retaliation against Section 232 steel and aluminum tariffs targets more than $6 billion worth of American products for an estimated total tax of approximately $1.6 billion.

Section 301, Chinese Products

Under the Trump administration, the United States Trade Representative began an investigation of China in August 2017, which culminated in a March 2018 report that found China was conducting unfair trade practices.

In March 2018, President Trump announced tariffs on up to $60 billion of imports from China. The administration soon published a list of about $50 billion worth of Chinese products to be subject to a new 25 percent tariff. The first tariffs began July 6, 2018, on $34 billion worth of Chinese imports, while tariffs on the remaining $16 billion went into effect August 23, 2018. These tariffs amount to a $12.5 billion tax increase.

In September 2018, the Trump administration imposed another round of Section 301 tariffs—10 percent on $200 billion worth of goods from China, amounting to a $20 billion tax increase.

In May 2019, the 10 percent tariffs increased to 25 percent, amounting to a $30 billion increase. That increase had been scheduled to take effect beginning in January 2019, but was delayed.

In August 2019, the Trump administration announced plans to impose a 10 percent tariff on approximately $300 billion worth of additional Chinese goods beginning on September 1, 2019, but soon followed with an announcement of schedule changes and certain exemptions.

In August 2019, the Trump administration decided that 4a tariffs would be 15 percent rather than the previously announced 10 percent, a $5.6 billion tax increase.

In September 2019, the Trump administration imposed “List 4a,” a 15 percent tariff on $112 billion of imports, an $11 billion tax increase. They announced plans for tariffs on the remaining $160 billion to take effect on December 15, 2019.

In December 2019, the administration reached a “Phase One” trade deal with China and agreed to postpone indefinitely the stage 4b tariffs of 15 percent on approximately $160 billion worth of goods that were scheduled to take effect December 15 and to reduce the stage 4a tariffs from 15 percent to 7.5 percent in January 2020, reducing tariff revenues by $8.4 billion.

In May 2024, the Biden administration published its required statutory review of the Section 301 tariffs, deciding to retain them and impose higher rates on $18 billion worth of goods. The new tariff rates range from 25 to 100 percent on semiconductors, steel and aluminum products, electric vehicles, batteries and battery parts, natural graphite and other critical materials, medical goods, magnets, cranes, and solar cells. Some of the tariff increases go into effect immediately, while others are scheduled for 2025 or 2026. Based on 2023 import values, the increases will add $3.6 billion in new taxes.

Section 301 tariffs on China currently account for $77 billion of the $79 billion in tariffs, based on initial import values. China has responded to the United States’ Section 301 tariffs with several rounds of tariffs on more than $106 billion worth of US goods, for an estimated tax of nearly $11.6 billion.

WTO Dispute, European Union

In October 2019, the United States won a nearly 15-year-long World Trade Organization (WTO) dispute against the European Union. The WTO ruling authorized the United States to impose tariffs of up to 100 percent on $7.5 billion worth of EU goods. Beginning October 18, 2019, tariffs of 10 percent were to be applied on aircraft and 25 percent on agricultural and other products.

In summer 2021, the Biden administration reached an agreement to suspend the tariffs on the European Union for five years.

Section 201, Solar Panels and Washing Machines

In January 2018, the Trump administration announced it would begin imposing tariffs on washing machine imports for three years and solar cell and module imports for four years as the result of a Section 201 investigation.

In 2021, the Trump administration extended the washing machine tariffs for two years through February 2023, and they have now expired.

In 2022, the Biden administration extended the solar panel tariffs for four years, though later provided temporary two-year exemptions for imports from four Southeast Asian nations beginning in 2022, which account for a significant share of solar panel imports.

In 2024, the Biden administration removed separate exemptions for bifacial solar panels from the Section 201 tariffs. Additionally, the temporary two-year exemptions expired and the Biden administration is further investigating solar panel imports from the four Southeast Asian nations for additional tariffs.

We estimate the solar cell and module tariffs amounted to a $0.2 billion tax increase based on 2018 import values and quantities, while the washing machine tariffs amounted to a $0.4 billion tax increase based on 2018 import values and quantities.

We exclude the tariffs from our tariff totals given the broad exemptions and small magnitudes.

Trade Volumes Since Tariffs Were Imposed

Since the tariffs were imposed, imports of affected goods have fallen, even before the onset of the COVID-19 pandemic. Some of the biggest drops are the result of decreased trade with China, as affected imports decreased significantly after the tariffs and still remain below their pre-trade war levels. Even though trade with China fell after the imposition of tariffs, it did not fundamentally alter the overall balance of trade, as the reduction in trade with China was diverted to increased trade with other countries.

from the White House

Fact Sheet: President Donald J. Trump Imposes a Temporary Import Duty to Address Fundamental International Payment Problems

PROTECTING THE U.S. ECONOMY AND NATIONAL INTERESTS: Today, President Donald J. Trump signed a Proclamation imposing a temporary import duty to address fundamental international payments problems and continue the Administration’s work to rebalance our trade relationships to benefit American workers, farmers, and manufacturers.

- President Trump is invoking his authority under section 122 of the Trade Act of 1974, which empowers the President to address certain fundamental international payment problems through surcharges and other special import restrictions.

- By taking this action, the United States can stem the outflow of its dollars to foreign producers and incentivize the return of domestic production. By increasing its domestic production, the United States can correct its balance-of-payments deficit, while also creating good paying jobs, and lowering costs for consumers.

- The Proclamation imposes, for a period of 150 days, a 10% ad valorem import duty on articles imported into the United States.

- The temporary import duty will take effect February 24 at 12:01 a.m. eastern standard time.

- Some goods will not be subject to the temporary import duty because of the needs of the U.S. economy or in order to ensure the duty more effectively addresses the fundamental international payments problems facing the United States, including:

- certain critical minerals, metals used in currency and bullion, energy, and energy products;

- natural resources and fertilizers that cannot be grown, mined, or otherwise produced in the United States or grown, mined, or otherwise produced in sufficient quantities to meet domestic demand;

- certain agricultural products, including beef, tomatoes, and oranges;

- pharmaceuticals and pharmaceutical ingredients;

- certain electronics;

- passenger vehicles, certain light trucks, certain medium and heavy-duty vehicles, buses, and certain parts of passenger vehicles, light trucks, heavy-duty vehicles, and buses;

- certain aerospace products; and

- informational materials (e.g., books), donations, and accompanied baggage.

- In addition, the following goods will not be subject to the temporary import duty:

- all articles and parts of articles that currently are or later become subject to section 232 actions;

- USMCA compliant goods of Canada and Mexico; and

- textiles and apparel articles that enter duty-free as a good of Costa Rica, the Dominican Republic, El Salvador, Guatemala, Honduras, or Nicaragua under the Dominican Republic-Central America Free Trade Agreement.

- In a separate Executive Order, President Trump also reaffirmed and continued the suspension of duty-free de minimis treatment for low-value shipments, including goods shipped through the international postal system, which will also be subject to the temporary import duty imposed under section 122.

- In addition to today’s actions, the President has directed the Office of the United States Trade Representative to use its section 301 authority to investigate certain unreasonable and discriminatory acts, policies, and practices that burden or restrict U.S. commerce.

ADDRESSING FUNDAMENTAL INTERNATIONAL PAYMENT PROBLEMS: The United States faces fundamental international payment problems, in particular a large and serious balance-of-payments deficit.

- As a result of its loss of domestic production, the United States must import much of what it consumes, sending U.S. dollars out of our own economy and overseas.

- A measurement for the U.S. balance-of-payments is the current account, which tracks the three ways a country can make money: (1) selling goods and services overseas, or the “trade balance of goods and services”; (2) return on investment or labor, or the “balance on primary income”; and (3) voluntary transfers, like remittances, or the “balance on secondary income.”

- The United States not only runs an overall current account deficit, but also a deficit in each component of the current account.

- The annual U.S. goods trade deficit exploded by over 40% during the Biden Administration, reaching $1.2 trillion in 2024.

- In 2024, for the first time in more than 60 years, the United States made less on the capital and labor it deployed abroad than foreigners made on the capital and labor they deployed in the United States.

- At present, more money is transferred out of the United States through remittances than money is transferred in.

- The situation is getting worse.

- In 2024, the United States maintained a current account deficit of -4.0% of gross domestic product (GDP), almost double the current account deficit of approximately -2.0% that prevailed between 2013 and 2019, and larger than 2019 to 2024.

- As a share of GDP, the 2024 current account deficit represented the biggest annual current account deficit since 2008.

- Compounding these challenges is the decline in the U.S. net international investment position.

- At the end of 2024, the U.S. net international investment position was $26 trillion, which was 89% of U.S. GDP. This means that if all of the obligations to foreigners that the United States has incurred were to come due today, and even if all of the foreign assets that the U.S. owns could be instantly deployed as payment, the United States would still end up needing to make payments equal to 89% of its annual economic output in order to meet its obligations. This represents the most negative net international investment position of any country on Earth.

- If left unaddressed, these fundamental international payment problems can, among other things, endanger the ability of the United States to finance its spending, erode investor confidence in the economy, distress the financial markets, and endanger U.S. economic and national security.

CONTINUING TO UTILIZE TARIFFS TO PROTECT U.S. INTERESTS: Tariffs will continue to be a critical tool in President Trump’s toolbox for protecting American businesses and workers, reshoring domestic production, lowering costs, and raising wages.

- The Supreme Court’s disappointing decision today will not deter the President’s effort to reshape the long-distorted global trading system that has undermined the economic and national security of our country, and contributed to fundamental international payment problems.

- Since Day One, President Trump has challenged the assumption that the United States must tolerate the distorted and imbalanced global trading system.

- The President’s trade policy brought the world to the negotiating table on our terms.

- As a result of the President’s tariffs, major U.S. trading partners covering more than half of global GDP have agreed to historic trade and investment deals to open new markets for U.S. exports, promote manufacturing reshoring, and bring reciprocity and balance to our trade relations.

- These deals are creating high-paying American jobs, boosting U.S. manufacturing and technological leadership, and will deliver massive returns for American workers and families for decades to come.

- In particular, the United States will continue to honor its legally binding Agreements on Reciprocal Trade. The United States expects the same commitment from its trading partners. While the domestic legal authorities to impose future tariffs will change, the overall direction of travel for the United States—reshoring domestic production and expanding market access abroad through a combination of tariffs and deals—will not.

- Today’s action will continue to protect the national interests of the United States by addressing the balance-of-payments deficit to further usher in America’s Golden Age.

from — Kotkiewicz, J. (2026, February 21). Fact Sheet: President Donald J. Trump imposes a temporary import duty to address fundamental international payment problems. The White House.

This is one of the words/ phrases you can’t say in the new Trump Regime. See a comprehensive list at the Forbidden Words Project.

image: rollermagic © Holly Troy 2.2026

There’s nothing “free” about banning words or ideas.

from — Connelly, E. A. (2025, December 22). Federal Government’s Growing Banned Words List Is Chilling Act of Censorship. PEN America.

Climate Science Legal Defense Fund

see Silencing Science Tracker — https://silencingscience.org/

Discover more from holly troy ~ sacred folly

Subscribe to get the latest posts sent to your email.

Trump has fucked the World / again and again with his / illegal actions

LikeLiked by 1 person